An Undervalued Global Water Technology Company Institutional Investors Are Buying

Environmental challenges and aging infrastructure are all tailwinds

You can’t do deep dives into each of the 5,000+ stocks traded on the US stock exchanges.

This is why I look for stocks with growth potential by looking at their charts first. Humans are visual creatures. It takes us a second to spot a stock with strong trendline patterns.

Plus all information about a public company is in its stock chart. You may misinterpret it but it’s still there.

This chart stopped me in my tracks.

3 things make it unusual:

It was in a free fall due to the tariff situation in April 2025

It came back in no time by forming a V-shaped bottom (fundamentals were below the price)

There are institutional buy zones all over the place (the stock is still undervalued).

The company is Xylem, a global water technology company.

Let’s dive deep into it.

Focus on water and wastewater infrastructure

Xylem (ticker XYL) provides solutions for transporting, treating, analyzing, monitoring, and returning water.

It’s active in public utilities, industrial, commercial, agricultural, and residential settings. Xylem’s strong point is working across the full water cycle:

Clean water delivery

Wastewater removal, transport, and treatment

Instrumentation for analytics and monitoring

Xylem is a spin-off of the water-related business of ITT Corp. we discussed recently. ITT is a diversified industrial manufacturer with business operations beyond water (industrial pumps, valves, switches, connectors, and products for vehicles).

Xylem focuses entirely on water and wastewater infrastructure. It’s headquartered in Washington, DC and present in 150 countries.

The company organizes its revenue into four core segments. Each has different end markets and dynamics:

1. Water Solutions and Services (30% of revenue): Treatment, transport, and assessment services solutions. These focus on ongoing support like wastewater purification, reliable water flow with pumps, and non-invasive leak detection to maintain and optimize water systems.

This is a service-oriented segment.

The main operations are in the US (80%). Utilities, industries, and municipalities are the main clients. Xylem has an extensive service network which produces recurring revenues for this segment.

2. Applied Water (20%): Solutions for residential, commercial, industrial, and agricultural water use. They include pumps, valves, heat exchangers, controls, and dispensing equipment.

Operations are in the US (50%), Western Europe (20%), and other locations.

3. Water Infrastructure (30%): Products for the transportation and treatment of water for municipal, utility, and industrial water systems. The products are pumps, filtration and treatment equipment, and controls.

The operations in this segment overlap with Water Solutions and Services but they lean toward product offerings, not services.

Operations are almost evenly split between the US (35%) and Europe (35%) and the rest of the world.

4. Measurement and Control Solution (20%): Technology solutions for water and energy. The focus is on meters, analytics, sensors, monitoring systems, and software and data services for utilities and industrial customers

Most of the operations in this segment are in the US (65%).

In 2023 Xylem acquired Evoqua for $7,5 billion in an all-stock transaction. It was a strategic deal that reinforced Xylem’s positioning.

Xylem was strong in pumps, transport, metering, and analytics. Evoqua’s services focus on purifying, recycling, and managing industrial and municipal water. The combined company became a full-stack water solutions provider from moving water to monitoring and recycling it.

The anticipated reduction in the operating expenses of the resulting company was $140 million.

Xylem’s opportunities for growth

There are tailwinds for Xylem.

Water scarcity is the first. It’s a rapidly deteriorating global issue. UNICEF says:

“Some 700 million people could be displaced by intense water scarcity by 2030.”

Smart water management is crucial now that we have extreme weather and a large number of natural disasters.

Xylem sells pumps, analytics, digital monitoring systems, and treatment technologies for water. The more scarce water becomes, the higher the demand for Xylem’s products and services.

Second, emerging contaminants are a group of chemicals that have recently been recognized as risks to human health or the environment (pharmaceuticals, personal care brands, microplastics).

It’s a big opportunity for Xylem. The company offers

Granular activated carbon (Westates brand) adsorbs chemicals, pharmaceuticals, and microplastics from water. It’s used in municipal filtration systems and mobile units for emergency contaminant removal.

Ion resins exchange harmful ions from chemicals with harmless ones. The resins are applied in single-pass systems for groundwater treatment.

Advanced oxidation systems (Wedeco brand) break down emerging contaminants like micropollutants and taste or odor compounds. The systems are used in wastewater plants for oxidation of pharmaceuticals and algae byproducts.

In addition, many industries must meet strict quality standards for water reuse. The above-mentioned products Xylem sells remove contaminants from water.

Another big opportunity for Xylem is cooling data centers. The company says optimization of water solutions for data centers will help operational efficiency, environmental responsibility, and cost control in this growing segment.

Xylem’s brand is thriving due to the strong partnerships and relationships with clients. These are based on long-term contracts for pumps, treatment, and digital monitoring.

They’re all part of a critical infrastructure. Switching providers is costly and risky. Hence Xylem’s recurring revenue.

For example, recently Xylem closed these deals:

A three-year contract was signed in Italy to “revolutionize the region’s [Tuscany’s] water supply system from source to tap”. It includes meter data analytics, real-time leak detection modules, and predictive maintenance tools.

A digital transformation deal was signed in Immokalee, Florida, US. The goal is to track water pressure, monitor water quality, integrate potable water distribution, and collect and treat wastewater.

Xylem is still a growth stock

Xylem has been around since 2011 after it spun off from ITT. It’s a profitable business with solid financials:

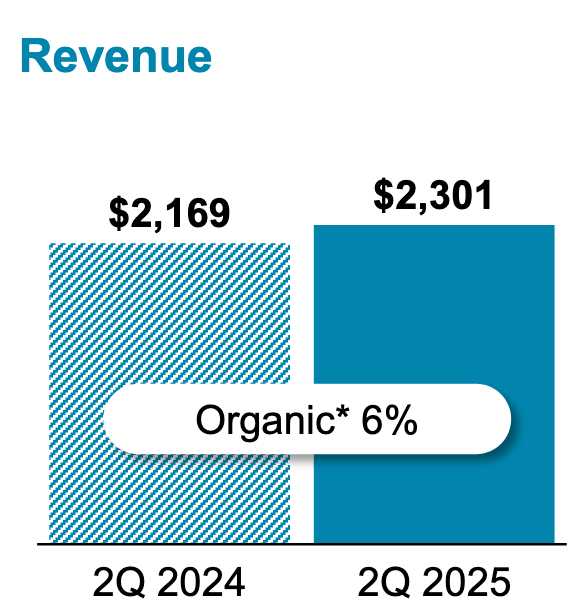

Revenue up 6% YoY

Annualized revenue up 4%

Long-term debt $1,98 billion

Free cash flow $946 million

Dividend yield 1,08%

The numbers aren’t phenomenal, and Xylem won’t turn into a ten-bagger by next year. However, it’s still a growth stock with several tailwinds.

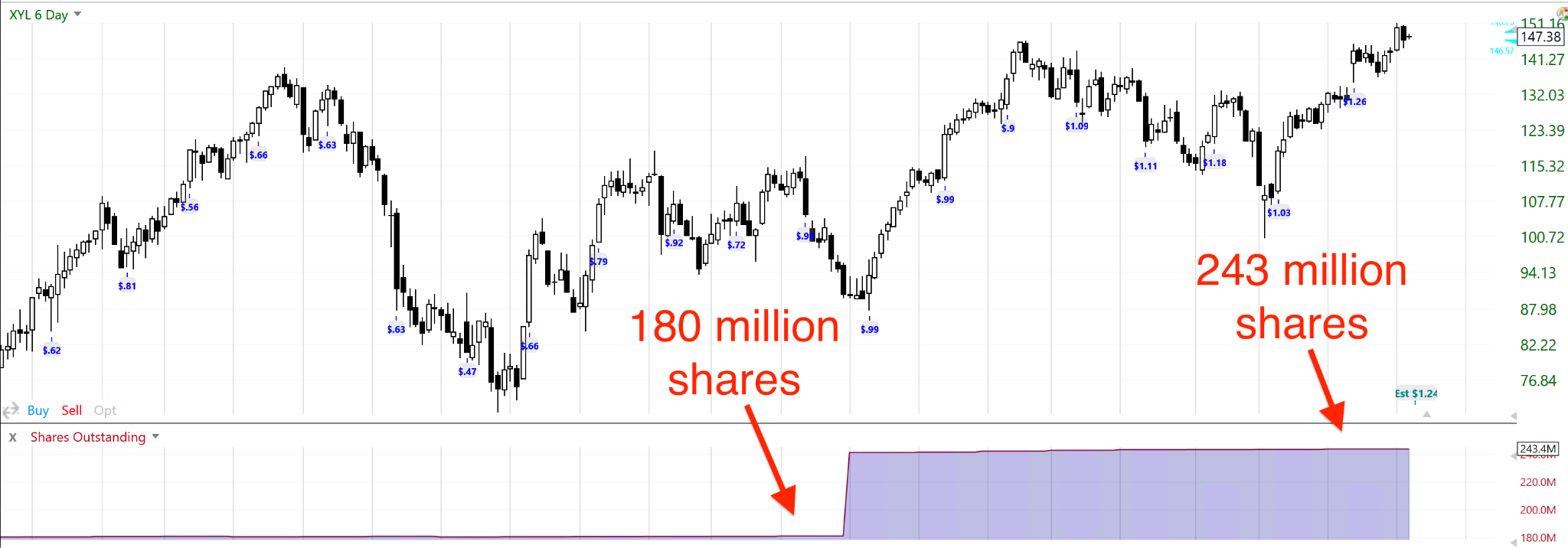

Xylem doesn’t abuse dilution. It had 180 million shares outstanding before the Evoqua acquisition in 2023. Before the acquisition was paid in Xylem stock, the total share count increased to 240 million.

Now two years later, Xylem has 243 million shares. Dilution has close to 1% a year since 2023.

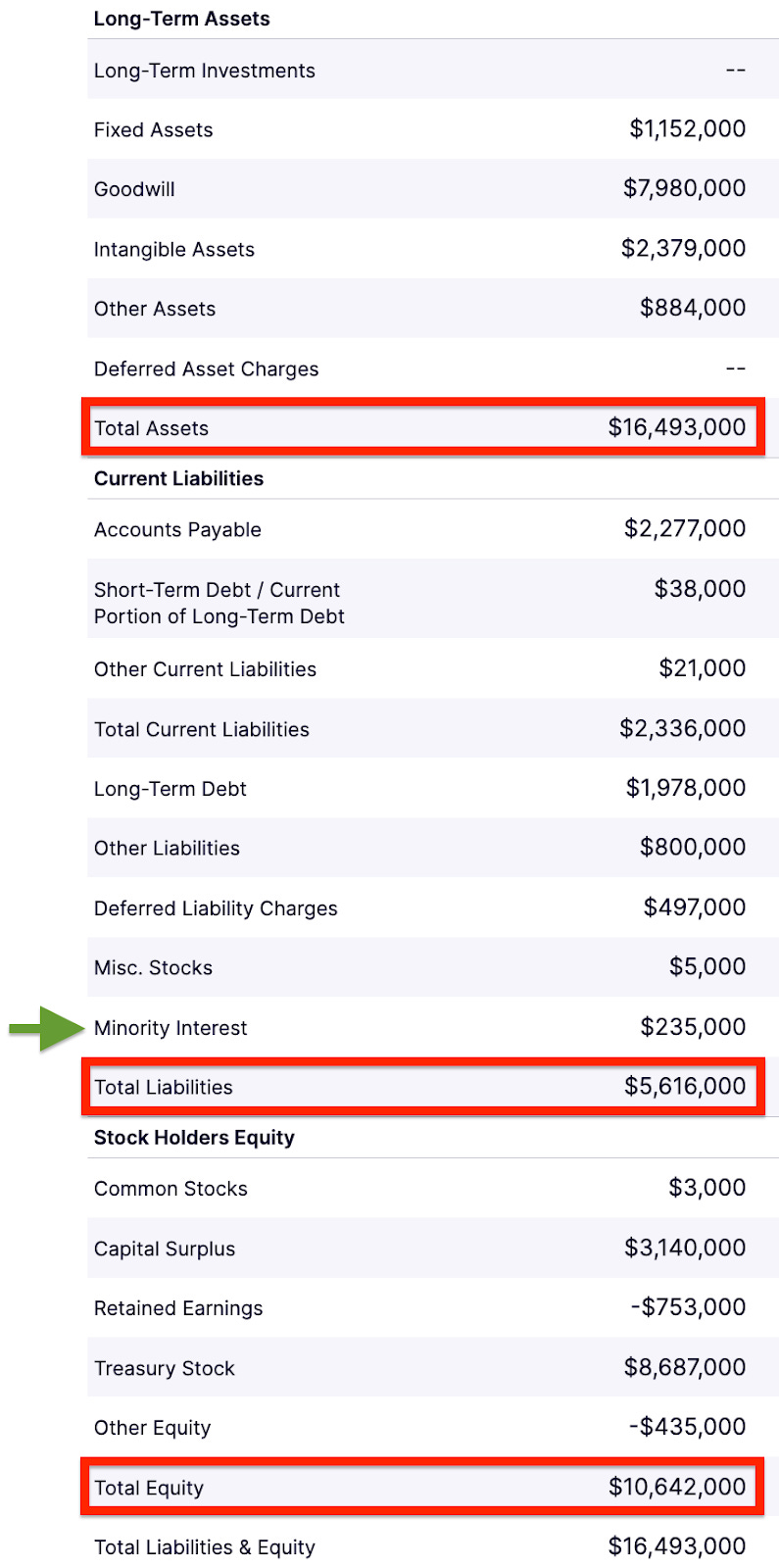

Xylem has a strong balance sheet that reflects a conservative attitude to leverage. But you should notice one thing.

The Evoqua deal resulted in a “minority interest” for Xylem. This means that part of the company’s profits goes to outside investors.

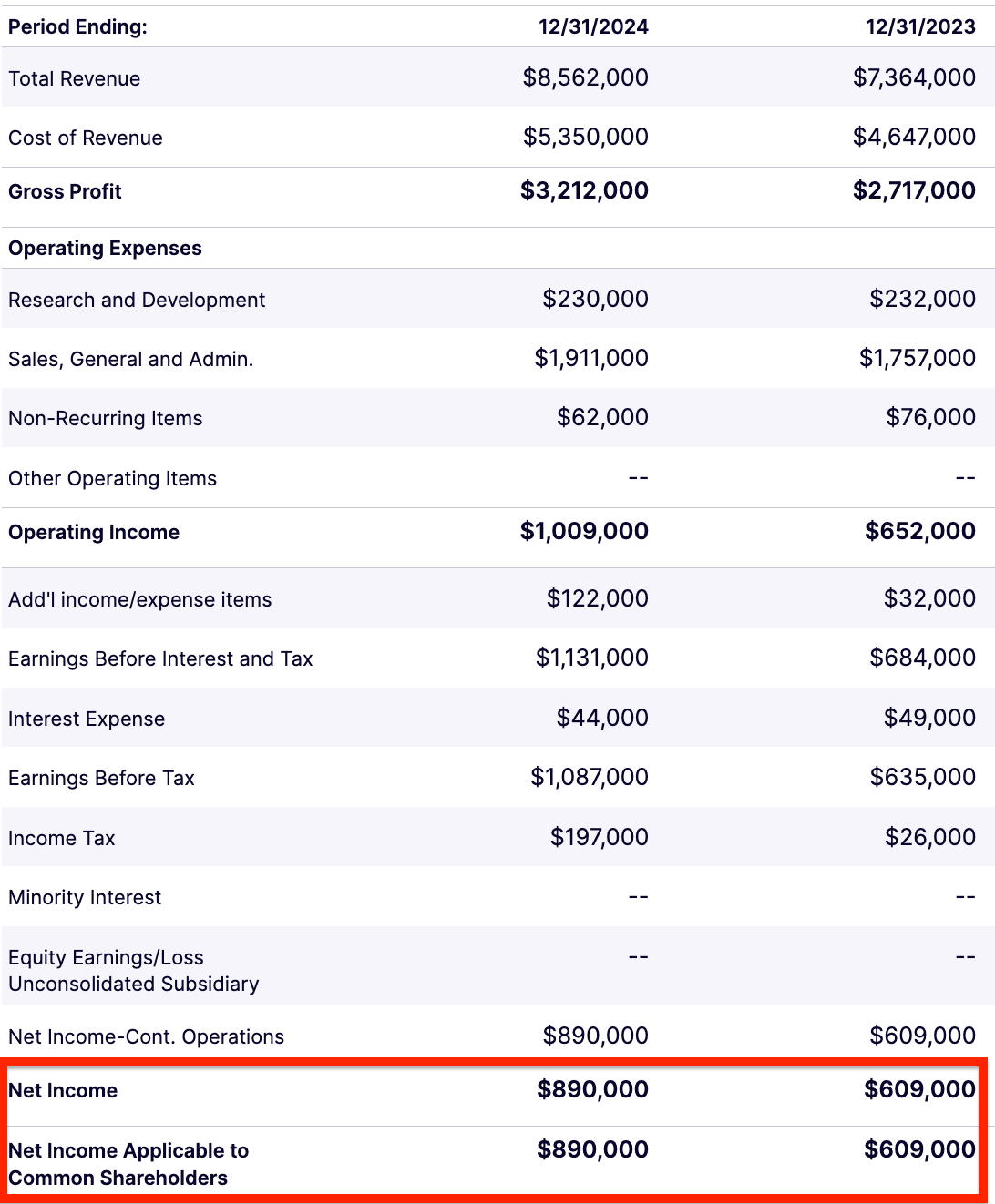

The size of minority interest is $235 million. Xylem’s reported earnings ($890 million in FY 2024) already account for it.

The $235 million figure is significant compared to the earnings. But it’s tiny compared to Xylem’s market cap ($36 billion). So the minority interest doesn’t significantly affect shareholder value.

Minority interest doesn’t mean Xylem loses cash. The interest is not “eating profits.” The cash flow attributable to Xylem shareholders remains strong because the company includes 100% of the financial results of Evoqua’s operations.

Anyway, Xylem’s earnings in 2024 grew more than $235 million compared to 2023, which shows the minority interest isn’t a concern for overall profitability.

Significant headwinds are unlikely

Xylem looks good in the near term, both from the fundamental (financials) and technical (stock chart) perspectives.

But what could impair its operations long-term?

The first point is the tariff wars. They’ve affected Xylem’s operations but the company has been able to mitigate their impact by hiking prices and managing its supply chains.

Other potential headwinds:

Reduced industrial, municipal, and construction spending across the world. It’s unlikely given that much of the world’s municipal infrastructure is aging in both the US and Europe.

Regulatory changes could increase compliance costs or limit market access. The company already optimizes water solutions. Stricter compliance means optimizing the already optimized solutions. I’d expect Xylem to pass the increased costs on to its customers.

Raw material or supply chain constraints could lead to price spikes or shortages in metals, plastics, or electronic components. Yes, this will initially hurt the margins.

So far Xylem has survived the Covid crash, the 2022 bear market, and the 2025 flash crash while growing its earnings.

I’m optimistic about Xylem.

The takeaway

Not every good company has to be an aggressive growth stock.

Xylem sells products and services for water management. What it does is essential.

The current global trends related to environmental challenges, aging infrastructure, and technological advances make Xylem an irreplaceable partner for water management solutions.

Xylem is a good stock for the conservative part of your portfolio.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.

P.S. Companies providing essential services like water solutions have long-term multi-bagger potential. If you want to learn more of such companies, hit Subscribe.

Interesting company. I've seen them at several trade shows. Not an easy industry to enter and they're apart of a huge infrastructure component.

Like the sound of Xylem, Denis. A company trying to do good and make money at same time - this is the healthy side of capitalism. Cheers, мой друг))