This Quantum Computing Company Just Went Public With a Wildly Overpriced Stock

I’m watching it from the sidelines

I invested in Lyft in 2021 and watched the stock go down by 75%. That taught me a lesson: Never invest in a company that just went public.

Companies go public to raise capital and expand. There are occasional gems that are already profitable like Google and Visa. They didn’t tank after they started trading on public exchanges.

But most young public companies are unprofitable, and the market could buy into the hype initially. If there’s no clear growth direction, the market will eventually start to ask where the money is. That was my dear Lyft stock.

Now this year we’ve been hearing increasingly more of three huge private companies: SpaceX, OpenAI, and Anthropic. They’ve overshadowed other IPOs (Initial Public Offerings).

One of them is Quantinuum (QNT), a company that develops and sells quantum computers. It IPO’d this week on Thursday.

Quantum computers will solve numerical problems even the most powerful supercomputers can only solve in thousands or millions of years. The potential of this new technology is enormous. Quantum computers could help us optimize delivery routes, facilitate drug discovery, and improve financial analysis. Some people even speculate that quantum computers will break blockchain encryption and endanger Bitcoin.

But potential doesn’t automatically mean the technology has matured. Most quantum computing companies are deep in R&D even though some are already selling their hardware or access to their machines through the cloud.

Where does Quantinuum stand and should you buy its stock?

Let’s answer this question.

Quantinuum is doing exciting stuff that cannot scale up

Quantum computers run on qubits which can be simultaneously in 0 and 1 states, in contrast to the traditional bits that are either 0 or 1.

The issue with qubits is they’re fragile. Their states can be destroyed by vibrations, electromagnetic fields, or temperature changes.

So physical qubits are noisy. You can’t run quantum computations on them. You need logical qubits to build a useful quantum computer.

A logical qubit is an array of physical qubits that can perform error correction. For this to work, logical qubits need to keep their state from collapsing longer than the underlying physical qubits.

This is called breakeven.

If a logical qubit is worse than the underlying physical qubits, error correction isn’t helping. If it’s better, you actually get a useful result from the computations.

Quantinuum’s biggest claim is the demonstration of 48 logical qubits.

That many logical qubits is a huge number at present. Absolutely insane. Most quantum computers built until now have demonstrated no logical qubits at all.

Quantinuum’s success is due to the trapped-ion technology it uses. Similarly to IonQ (IONQ), the ions are in a vacuum where they physically move (although the companies control the ions by different means). Any ion can potentially go near and sense any other ion. This is all-to-all connectivity, and it’s good for error correction.

By contrast, quantum computers based on superconductors have qubits fixed on a chip. The qubits are wires of a superconductor material. They can’t move. A qubit can only sense its nearest neighbors. To sense a distant qubit, it needs to propagate a signal through several other qubits. That signal will be affected by noise and need to be corrected more.

This is the reason why quantum computers based on superconductors have a 1,000 to 1 ratio for the number of physical to logical qubits. For the trapped-ion systems built by IONQ, the figure reduces to 32 to 1.

Quantinuum reported 48 error-corrected logical qubits mapped across 98 physical qubits. It’s almost a ratio of 2 to 1.

What the heck?

We need to go deeper into the technology behind Quantinuum’s “breakthrough.”

You’d expect a fully fault-tolerant quantum computer to fix errors as soon as they’re detected during computations. That’s not what Quantinuum does.

Its demonstration of 48 logical qubits relies on post-selection. First, the system performs a calculation. Then, if it detects an error, the system filters out and discards the corrupted runs at the end.

But quantum computations can take weeks or even months. You can’t afford to discard a ton of corrupted runs at the end when your calculation is so time-consuming.

Quantinuum is open about this. The acceptance rate (“correctness”) was 25% when it was using a 48 logical qubit state. But for more complex models like material simulation, the acceptance rate fell to 3,2%.

You have to discard more than 96% of your computations! This is not a demonstration of scaled, full fault-tolerance.

What Quantinuum did is still a great achievement for systems that don’t require too many physical qubits to build one logical qubit. The company designed a code for error correction that works specifically for 98 physical qubits and 48 error-corrected logical qubits.

That’s how technology should work in theory. Now let’s look at what could go wrong.

1/ Scaling up will likely hit a wall because Quantinuum relies on external laser arrays to manipulate qubit states. The lasers require extreme precision to hit specific moving atoms on a track.

You can still do that with a hundred qubits but what will happen when you scale them to millions? The laser control will grow exponentially complex.

2/ Quantinuum needs cryogenic liquids like helium.

It’s one more component that could mess up your computer’s operations.

Quantinuum doesn’t need extreme cooling to almost absolute zero like superconductors. It uses liquid helium to create a cryopumping effect. Technically, it’s a vacuum inside the quantum chip, but there are a few remaining gas atoms within the package. Cryopumping freezes out those atoms and reduces the pressure inside the chip. Colder atoms move more slowly and disturb the quantum states less.

To get to 15 K (-258 degrees Celsius), liquid helium is unavoidable. Quantinuum uses closed-cycle refrigerators. Once you add helium to your system, you no longer need a constant supply of it.

That’s for one quantum computer built using hundreds of qubits. Now imagine how much helium and how many refrigerators you need for a computer built on millions of qubits.

Quantinuum says in its Form S-1:

“Our operations require significant quantities of helium, a scarce and non-renewable resource, and the use and storage of helium subjects us to environmental, health, and safety risks.”

3/ Helium requires a refrigerator that takes up physical space.

This is not optimal for the deployment of quantum computers in submarines and aircraft.

However, Quantinuum sells access to its quantum machines through the cloud, similarly to other quantum computing companies. If you don’t want to buy its hardware, then refrigerators don’t matter to you as a client.

To sum up, Quantinuum is an interesting company.

But given that its roadmap for scaling up is not clear, the initially expected $12,7 billion IPO valuation (upsized to about $15 billion) was too rich for me.

What’s wrong with Quantinuum’s valuation

Analyzing Quantinuum’s financial position in isolation doesn’t make sense.

The entire quantum computing industry is going through a period of unprecedented growth. Some companies have truly insane valuations, and I agree with the investors who call some of them dogsh!t wrapped in catsh!t.

Look at some of their current Price to Sales:

Quantum Computing (QUBT): 3,955

Rigetti Computing (RGTI): 1,198

D-Wave Quantum (QBTS): 454

Quantinuum (at IPO): 502

IonQ (IONQ): 207

I prefer to compare Quantinuum with its closest competitor (IONQ) in terms of the technology because they both use trapped ions. Moreover, IONQ is the largest company by market cap ($26,8 billion), annual revenue ($130 million in 2025), and R&D spend ($125,7 million).

So, here comes a financial reality check for Quantinuum vs IONQ.

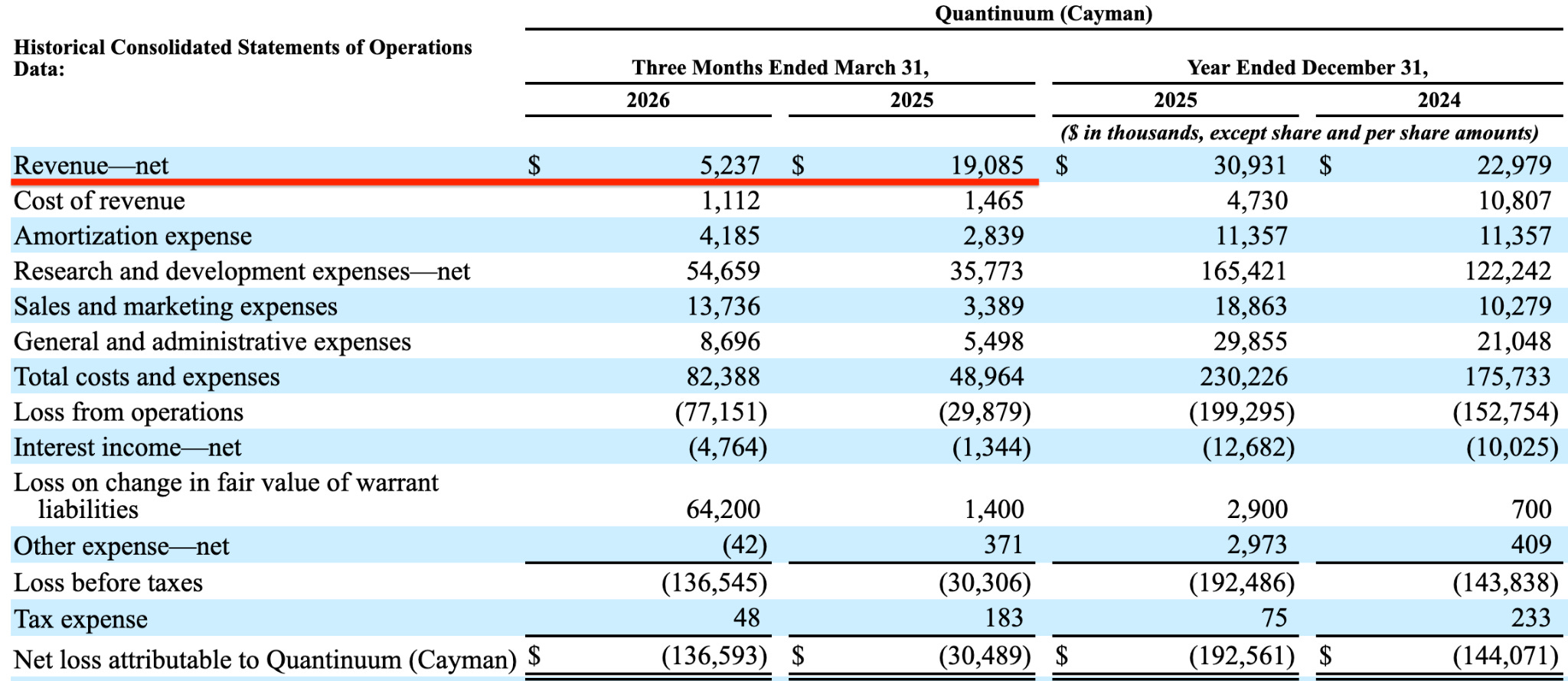

Quantinuum’s 2025 revenue was $30,9 million, and it has a massive customer concentration risk. Its main customer, Japan’s national research institute RIKEN, accounted for 63% of 2024 revenue and 60% of 2025 revenue.

Quantinuum has relatively low revenue growth among quantum computing companies. Its annual revenue is up “only” 35% YoY but Q1 2026 revenue is down 73% YoY. This is a direct consequence of the reduced spending by RIKEN which only contributed 7% to Quantinuum’s revenue in Q1 2026.

So the Price to Sales of 502 at IPO this week appears overblown.

Before you invest in Quantinuum, ask yourself when it’s going to diversify its customer base.

By contrast, IONQ has no such customer concentration risk. 60% of its revenue comes from commercial, 35% from international, 5% from government and academic customers.

IONQ has high revenue and backlog growth. Its annual revenue is up 202% YoY, quarterly revenue is up 755% YoY, and backlog is up 554% YoY.

IONQ’s valuation appears more reasonable. The current Price to Sales of 207 is the lowest among quantum stocks, while the forward Price to Sales is 97 for 2026.

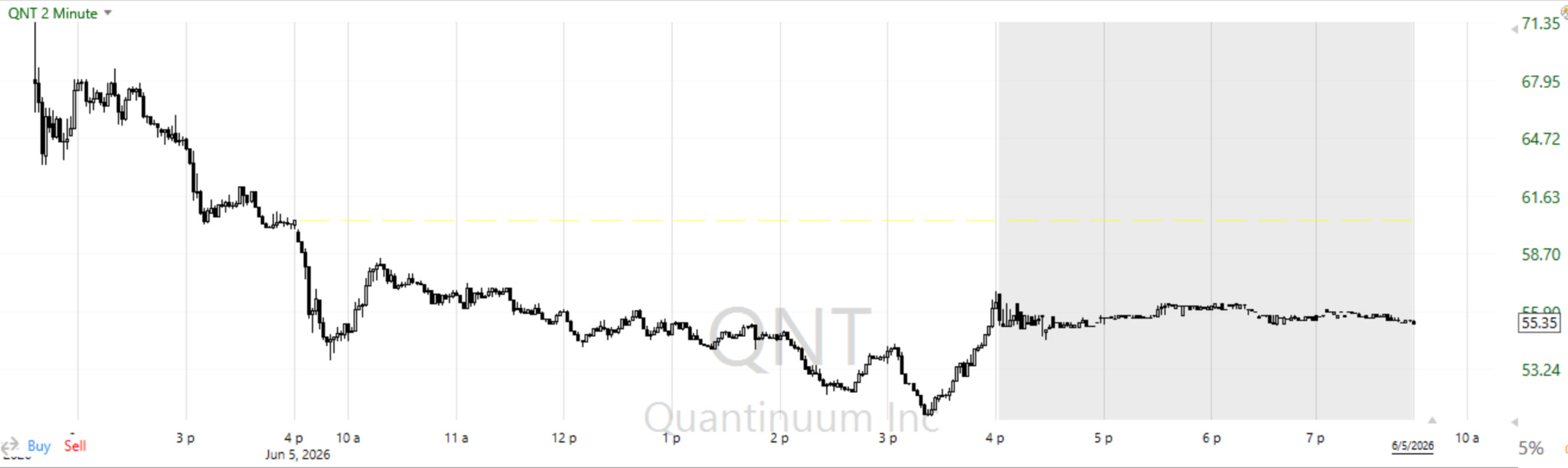

Here’s what Quantinuum stock did this week.

On Thursday, there was a delay in trading, supposedly due to a massive oversubscription (20 times, believe it or not). Investors wanted more stock than was available. So Quantinuum added 1,5 million shares in addition to the 26,5 million shares it had planned to sell originally.

This is weird because the stock chart shows a continuous decline in price on both days. I can’t find signs of a massive demand for Quantinuum stock. If it really was there, the selling overwhelmed the buying, and the stock went down anyway.

Quantinuum stock over the past two trading days:

June 4: Open $68,00, close $60,37

June 5: Open $59,80, close $55,35

In total, the stock is down 18,6%.

And who could be selling? Early investors and underwriters (banks that helped Quantinuum IPO). It’s not hard to create hype around a stock and offload your shares while everyone else is buying into a company with an uncertain future.

We have no idea what Quantinuum’s fundamental value is after just two trading days. It could soar if investors get excited. But I think it will tank as the hype evaporates and early investors dump their shares.

I’m going to wait for things to calm down first. There will be enough data after several quarters to make a decision if it’s worth owning Quantinuum.

Final words

I admit I’m biased because I already own IONQ. And I’m not trying to say Quantinuum is doomed. It could actually be the main contender for useful quantum computers.

However, in my view, IONQ is the most obvious leader in quantum computing at this point.

Yes, it has its own challenges. It also uses liquid helium for cryopumping its chips.

Additionally, IONQ hasn’t demonstrated logical qubits yet. Investors are anticipating its 256 (physical) qubit demonstration later this year. The question is: How many logical qubits will that be?

IONQ is targeting 80,000 logical qubits by 2030.

IONQ decided to pivot away from laser control because scaling will become unsustainable. The goal is to use chip-based electronic control, which is a clear path to scaling. IONQ is on track thanks to the recent acquisition of Oxford Ionics.

The next step is to acquire Skywater (SKYT). It’s a semiconductor foundry accredited by the US government as a Category 1A Trusted Foundry. It makes chips domestically. SKYT has a number of customers, and IONQ is one of them.

The SKYT acquisition has already been approved by SKYT shareholders and is currently being reviewed by the Federal Trade Commission. If the deal goes through, IONQ will become a vertically integrated developer and manufacturer of quantum computers.

We should always be ready to change our minds if R&D and financials start telling a different story.

But right now, I’m betting on IONQ and watching Quantinuum from the sidelines.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.

P.S. The potential of quantum computing is comparable to AI.

I keep an eye on quantum stocks to find early leaders in this new technology.

If you want to uncover them before the market does, hit Subscribe.

I like to hear about the underlying technical developments. Few are better positioned to describe them than you, Denis

I bought the Coinbase IPO and never recovered the losses. I am very skeptical about Quantum computing at its current stage.