Despite the Recent Volatility, I’ve Held All My Stocks and Added One New

It’s paying off now that the market is recovering

2026 will go down in history as a year of insane volatility.

Gold, silver, oil, stock, and Bitcoin prices have been unstable AF. The people trading on insider information have made a pile of money.

Us retail investors? We’ve probably made a bit less. But it’s not the end of the world because asset prices converge to their fundamental values over a long time frame.

This is why the only meaningful way of becoming wealthy from investing is to be in the market long-term. This means not giving in to panic selling when the market goes gaga.

I haven’t sold anything since September 2025. Some of my stocks have experienced crazy swings. But because my investment thesis hasn’t changed, I still hold them.

Here’s an update on my positions (and one new position).

1/ Pagaya Technologies (PGY)

PGY is a second-look tool for loan applications.

Banks evaluate loan applications based on your FICO score. This is a rigid framework that overlooks good borrowers. If your FICO score is a few points below a threshold, the bank can reject your application.

If that happens, your application goes to PGY that uses AI to reevaluate it based on your credit history, education, cash flow, spending habits, and so on.

If the bank approves your loan application, PGY will take it off the bank’s balance sheet, bundle it with other loans, and sell them to insurance companies, financial services companies, etc.

PGY’s service is to evaluate loans and bundle them into asset backed securities to sell them to those investors. PGY’s business is the network of banks and institutional investors it keeps for financial transactions.

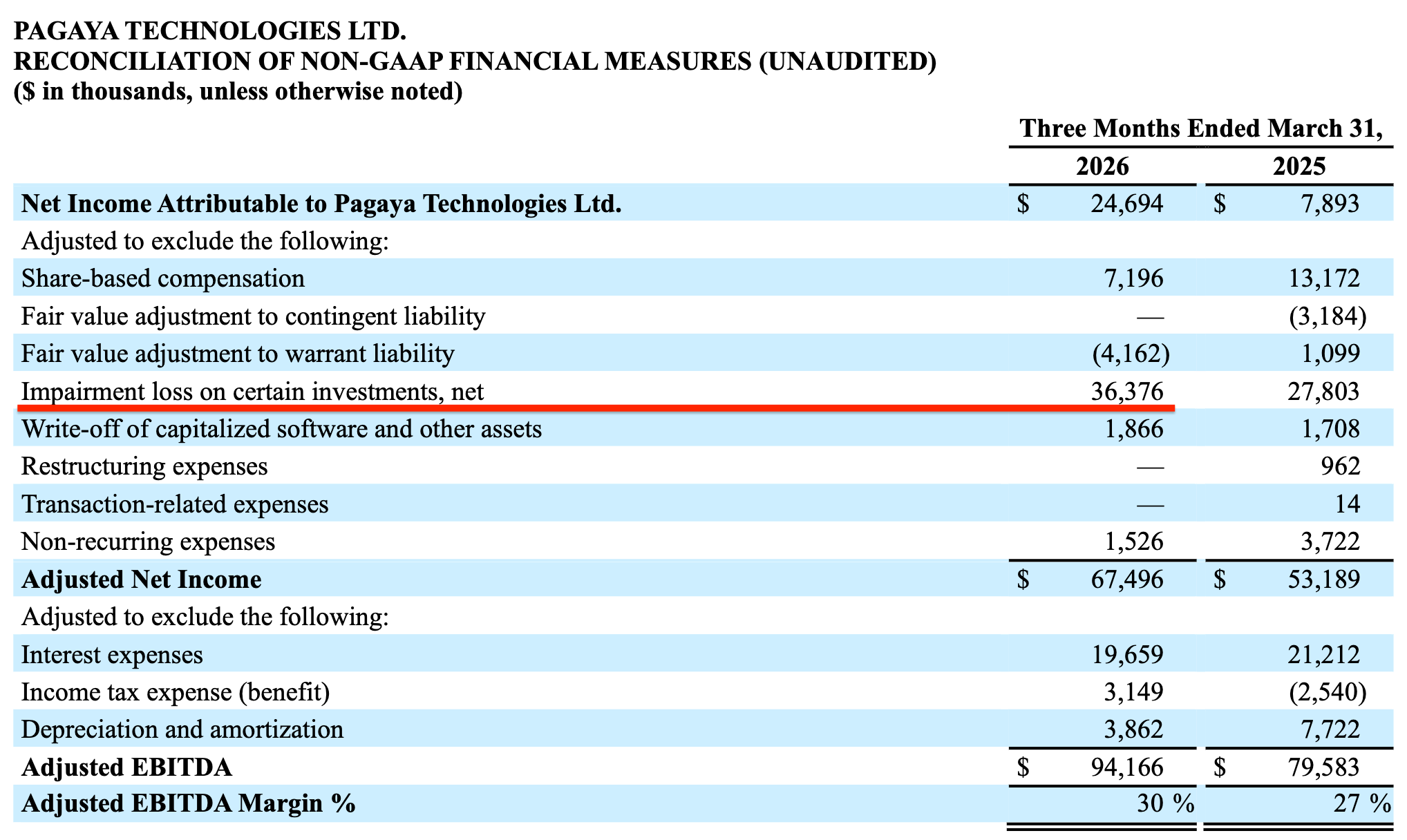

Financials from Q1 2026:

Revenue (and other income such as interest) up 10% YoY

GAAP net income up $25 million (5th consecutive profitable quarter)

Network volume up 9% YoY

Impairment loss $36,3 million

Two points deserve attention:

Credit-related impairments relate to defaults on the loans PGY recommends for origination. PGY is obliged to hold them on its balance sheet (up to 5%) in accordance with risk retention rules.

The losses are inevitable and they’re naturally a negative for the company. However, PGY takes them into account when issuing guidance.

Total 2026 impairment losses are projected to be between $100 million and $150 million, in line with the 2025 figure.

$36,4 million in Q1 falls within that range.

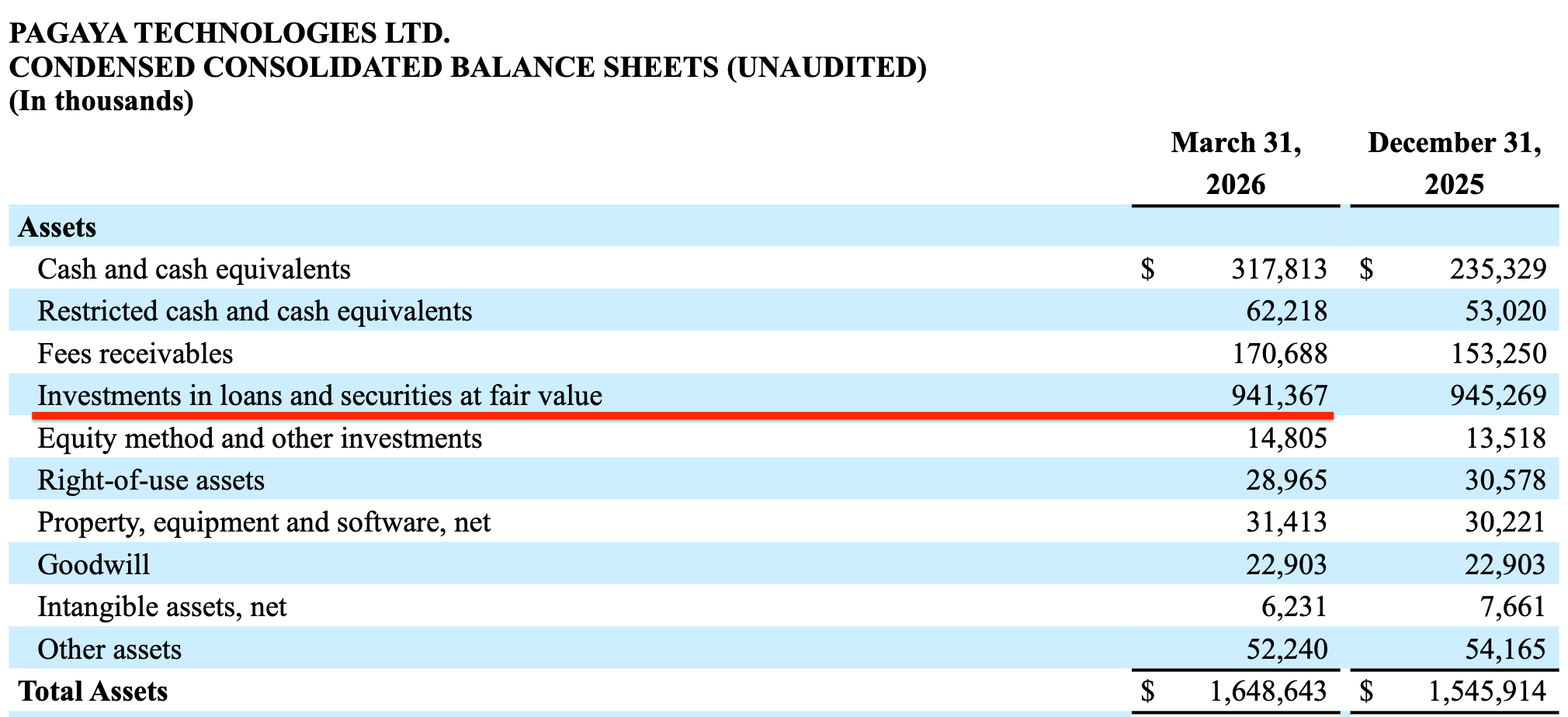

The second point is PGY’s interest income has soared by 130% YoY.

Where does it come from?

PGY holds high-interest securities (bonds) it also sells to other investors. The “Investments in Loans and Securities” on its balance sheet was worth $941,3 million as of Q1 2026.

PGY is collecting interest from these bonds.

But there’s a trade-off.

The loans are risky. While the total impairments were $36,4 million last quarter, interest income was $17,7 million.

This income appears smaller than the losses but we should note that the impairments don’t all come from those high-interest bonds. Interest income is up 130% while the impairments are roughly the same as a year ago ($36,4 million).

This means PGY is benefitting from the currently high interest rates.

PGY also onboarded 4 new partners last quarter:

Global Lending Services: To improve efficiency of auto lending

Upstart: PGY bundles its loans into asset backed securities

Sezzle: Buy now, pay later

Flex Pay: Buy now, pay later

PGY is also negotiating with regional banks to add them to its network.

Finally, PGY’s main revenue comes from three segments: Personal loans, Auto loans, and Point of Sale.

Personal loans are the biggest revenue source (63%) but Auto is catching up. In Q1 2026, PGY attracted $2,1 billion in funding from institutional investors.

As of Q4 2025, PGY has been exiting riskier market segments like Single Family Rentals which are becoming harder to finance due to high interest rates.

It’s like PGY has sacrificed a bit of growth in a riskier market segment in exchange for the stability of its business. The market didn’t like its Q4 2025 report in February when the stock fell.

This time, PGY stock soared (but then lost almost all the gain during the trading day) as the business is resilient despite the stressed lending market.

The result is PGY has raised the 2026 GAAP net income guidance to between $110 million and $160 million (up from the previous $100 million - $150 million).

2/ Zeta Global (ZETA)

ZETA is a customer intelligence platform that has developed a new way of online marketing.

Online marketing used to rely on cookies. They’re anonymous trackers that follow you on the Internet. Advertisers had to guess it was the same person using different browsers on different devices, to show the consumer their ads.

By contrast, ZETA sees exactly who you are. It can identify you on different devices because when you log into a site to leave a comment, you are giving ZETA the permission to identify you and collect data on you.

Mind you, ZETA doesn’t know your name. It uses hashing functions to keep your identity in its database. So Denis Gorbunov probably looks like “a045h78k.” Nevertheless, ZETA can still track your behavior and help other brands launch and run their ad campaigns.

Financials:

50% YoY revenue growth

19th consecutive beat and raise guidance

Guiding to positive GAAP net income for 2026

Raising 2026 revenue guidance by $30 million

Raising adjusted EBITDA guidance by $6,3 million

For me, the most important result is the growth of its super scaled customers (those who generate more than $1 million in annual revenue for ZETA).

In Q4 2025, ZETA had 184 such customers and they accounted for 90% of ZETA’s revenue. In Q1 2026, ZETA already had 189 super scaled customers while the average revenue per such a customer grew to $1,7 million or up 21% YoY.

ZETA is still unprofitable, and the Marigold acquisition is the main reason.

ZETA paid $325 million for Marigold with the expectation of adding more than forty Fortune 500 companies and twenty out of the top 100 global advertisers as clients. A lot of those brands are present in Europe and Asia. This means ZETA can collect data on consumer behavior outside the US, and its potential outreach would be 2,4 billion identities (it’s currently 550 million).

While Marigold is helping ZETA boost revenue, its integration costs were the main reason for the net loss of $13,2 million in Q1 2026.

Marigold came with several software brands (Cheetah Digital, Selligent, Marigold Loyalty, etc.). Each brand has its own tech stack which ZETA needs to normalize and migrate into the Zeta Marketing Platform. Then ZETA needs to analyze the consumer signals it inherited from Marigold’s enterprise clients.

The good news is this is not a recurring expense. Once ZETA is done with the integration, the losses will stop.

To put this in perspective, ZETA’s revenue in Q1 2026 was $396 million, up 50% YoY, and up 29% YoY excluding Marigold.

Marigold contributed $55,4 million to the total revenue and helped raise full year guidance by $30 million.

ZETA’s platform Athena should also be mentioned here.

It’s Agentic AI that has a partnership with OpenAI which boils down to the fact that Athena can use OpenAI’s most recent models.

Athena is expected to be the main revenue driver over the next few quarters.

Here’s what ZETA CEO David Steinberg said at Q1 2026 earnings call about the adoption of Athena by a customer:

“Athena was a driver in one of the largest deals we have ever closed.

The customer is a leading global apparel retailer operating across multiple brands, each with unique customers and over 3,000 locations worldwide.

Zeta’s platform was purpose-built to handle the complexity required by the largest enterprise companies, and this customer was able to consolidate down from four vendors to one, Zeta.”

In other words, the customer fired three vendors to keep one, ZETA.

Athena became generally available on March 24, 2026. David also noted:

“Athena drove greater than 7X more agent interactions and accounted for over 60% of AI platform usage in its first week of general availability.”

3/ SoundHound AI (SOUN)

SOUN develops AI tools that understand context, intent, and natural language. It’s a speech-to-meaning engine whose responses seem human.

SOUN stands out for three reasons:

1/ It has the best voice AI in the market.

It’s been developing the technology since 2005 and only specializes in voice AI. Big Tech also has voice AI and could potentially develop this technology to the level of SOUN. I doubt it’s a priority for Amazon and others right now as they’ve gone all in on datacenters.

2/ SOUN AI is Agentic.

It can act on your voice commands. You could be driving your car and ask the AI to find a restaurant close to your location and book a table there.

3/ SOUN doesn’t raise privacy issues.

For example, you can also talk to Alexa but it has every intention of sharing your private data with Amazon. SOUN doesn’t belong to Big Tech and has no interest in selling or sharing your data.

Q1 2026 wasn’t the best for SOUN.

The market didn’t like it when SOUN CFO Nitesh Sharan announced he was leaving the company in April. The stock tanked 8% that day.

I see Nitesh’s departure as a neutral move for three reasons:

1/ He is staying as an advisor for a transition period. He’s not disappearing.

2/ He isn’t leaving for a competitor or because of a disagreement.

He is moving to a leadership role in the quantum computing company Quantinuum. Maybe he’ll be paid more. Maybe the new role is more interesting to him.

3/ He explicitly stated he’s going to remain a long-term shareholder.

So there was nothing that suggested a major conflict at SOUN. I held the stock.

The latest earnings report came out this week:

No debt

Revenue up 52% YoY

Cash balance $216 million

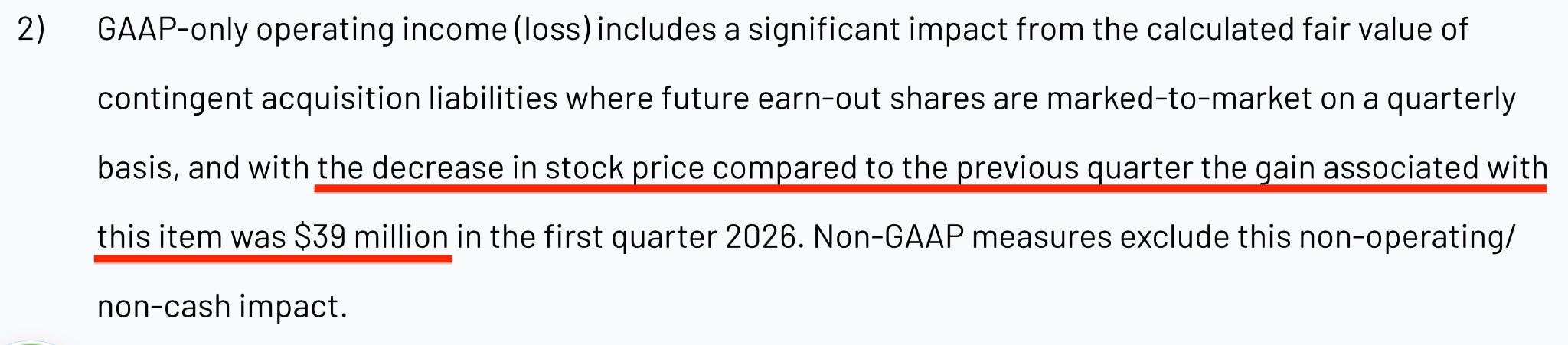

Net loss $25 million

The net loss included a gain from warrants in connection with the acquisition of LivePerson (conversational platform for customer engagement and messaging) settled in stock.

The warrants are the rights to buy SOUN shares at a lower than market price. It’s a liability with a variable value. The lower the stock price, the lower the warrants are worth (because fewer people will use them to buy a lower priced stock).

Because SOUN stock was falling most of Q1 2026, the warrants got cheaper. The net loss from operations would’ve been $64 million since the gain from a repricing of warrants was $39 million.

The stock fell 7% pre-market on Friday. I think it’s because of two reasons.

1/ To quote the report:

“First quarter expenses included certain non recurring charges such as true up costs from vendors.”

Although SOUN didn’t specify what that was, it was likely related to the datacenter and cloud infrastructure that SOUN pays for (the vendor wasn’t named).

This is also where the difference between GAAP gross margin (31,1%) and non-GAAP gross margin (49,7%) comes from.

2/ The market is expecting SOUN to become profitable in 2026.

SOUN didn’t mention this specific time frame. It just mentioned an “accelerated path to profitability.”

I’m not seeing any fundamental problem with the business. Saaspocalypse also affected SOUN while the company is growing revenue and has no debt.

I’m holding my SOUN shares and expecting profitability later this year.

4/ Nasdaq (NDAQ)

NDAQ’s last quarter shows the company is a major data and software firm beyond being a public exchange.

Financials:

Revenue up 14% YoY

Earnings up 33% YoY

Cash balance $515 million

1/ Index revenue is up 14% YoY. This is the licensing of NDAQ’s proprietary indexes. The company collects this revenue when someone buys the QQQ ETF or a Nasdaq-100 related product.

2/ Market Services revenue is up 13% YoY. It’s mainly the trading fees the exchange collects.

3/ Solutions revenue up is 14% YoY. This is Nasdaq Eqlipse and Adenza.

Eqlipse is a financial market technology platform. Every exchange needs trading, clearing, settlement, and data management but not every exchange can afford to develop these services, especially in developing countries.

So they simply sign up for NDAQ’s cloud software instead of building their own.

Adenza is a platform for risk management and regulatory reporting for capital markets. It manages the regulatory reporting for 90% of the world’s major banks.

The software is deeply integrated into how banks function. The cost of switching to another software provider is high.

For NDAQ this means a high client retention rate and steady revenue based on subscription fees.

Two more points are crucial:

NDAQ’s partnership with AWS allows the company to use Amazon’s massive datacenter presence across the world. Amazon’s capex is projected to be $200 billion this year.

For NDAQ, the capex is practically zero and it actually helps it expand its business to other exchanges by selling its financial technology. NDAQ is already doing this precisely because of Amazon’s global datacenter presence.

Recently, NDAQ also applied for 23/5 trading. Now it’s been approved by the SEC and will go live in December this year.

This move is for NDAQ to increase liquidity through its exchanges. It’s good for the company because it will capture the overnight volume from international investors. This means more trading fees.

As a NDAQ shareholder, I welcome this move. But as an investor who could take advantage of trading at night, I’m cautious. I buy and sell US stocks during market open, not when most investors are asleep.

Imagine trading 100 Apple shares with a small number of investors from Asia. So few participants will affect the stock price much more than during a normal trading day. Lower liquidity means larger price swings.

There are probably protection mechanisms in place. But for the time being, I’d stay away from buying and selling stocks when America sleeps.

NDAQ is a boring stock. It won’t grow 10x by next year but it’s a good investment for capital preservation.

It’s a mature company that pays dividends (yield 1,4%), grows its international presence thanks to its partnership with Amazon, and has $2,9 billion for share buybacks.

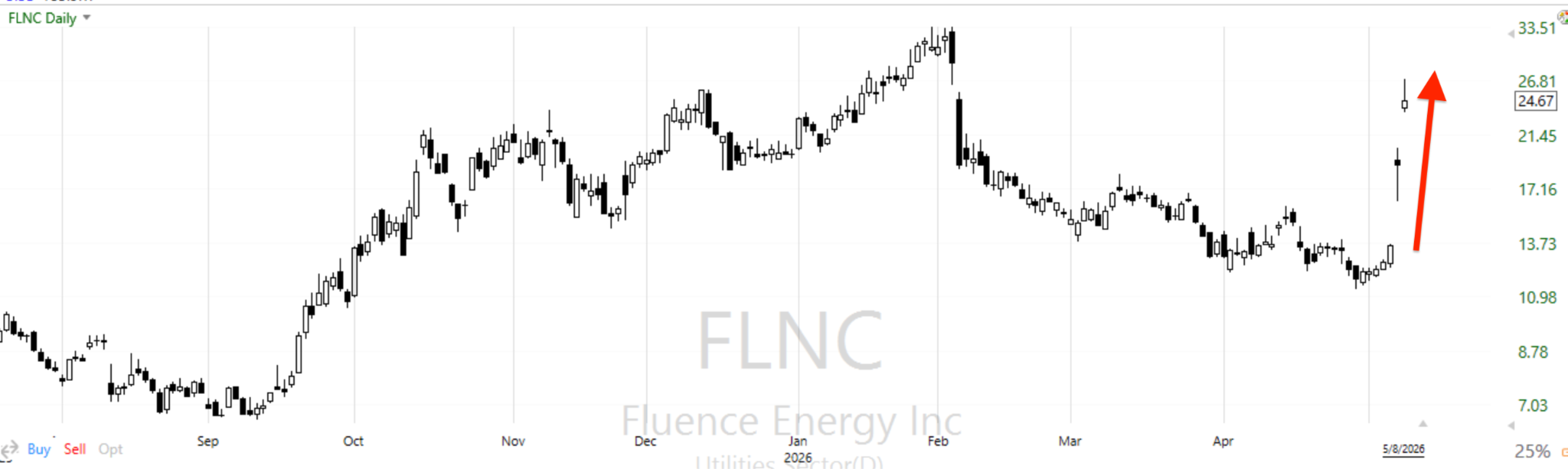

5/ Fluence Energy (FLNC)

FLNC provides battery-based energy storage systems for utilities like datacenters.

Datacenters don’t tolerate power spikes or interruptions. FLNC’s Gridstack Pro and Smartstack systems provide almost instantaneous backup power.

FLNC also sells software for optimizing energy use (Mosaic) and predicting battery failures (Nispera). As of Q1 2026 (ending December 31, 2025), they accounted for 5% of FLNC revenue. 95% came from battery solutions.

The company ran into problems in 2025 due to tariff uncertainty and staffing and technical calibration issues. Its revenue dipped and the stock fell by 80% from its peak valuation.

Toward the end of 2025, things improved. The earnings report in February 2026 was not spectacular, but it was also not a disaster. Nevertheless, FLNC stock fell by 34% on the earnings date and lost another 38% over the next two and a half months.

The main problem was margin compression due to unexpected expenses related to two projects. The adjusted gross margin was 5,6% in Q1 2026, down from 12,5% in Q1 2025.

For Q2 2026, I wanted to see margin improvement, ideally toward 13%. In addition, I wanted to see backlog growth. FLNC said in February it had expanded its pipeline by 30% to $30 billion while the backlog was $5,5 billion.

How much of that $30 billion is turning into contracted backlog?

Well, FLNC f*cking crushed earnings on May 6.

Revenue up 7% YoY

Net loss $29,2 million

Adjusted gross margin 11%

Order intake $2 billion

Backlog $5,6 billion

Total liquidity including cash $900 million

So yes, FLNC improved the backlog and gross margin. Now the entire 2026 revenue guidance is covered by the backlog.

It’s this line from the earnings report that warms my heart:

“Our customer expansion strategy is gaining momentum: we have signed master supply agreements with two hyperscalers and expect to convert our first order soon.”

I don’t care who the hyperscalers are (Microsoft, Meta, Amazon, etc.), this result shows the demand is there.

And just like that, the stock more than doubled within one week from the April lows.

The weird thing is UBS downgraded the stock to sell 5 days before the report.

The final point is the monetization of tax credits due to the One Big Beautiful Bill Act. FLNC manufactures its products in the US, which means they qualify for tax credits.

Things are pointing in the right direction for FLNC. I’m a shareholder.

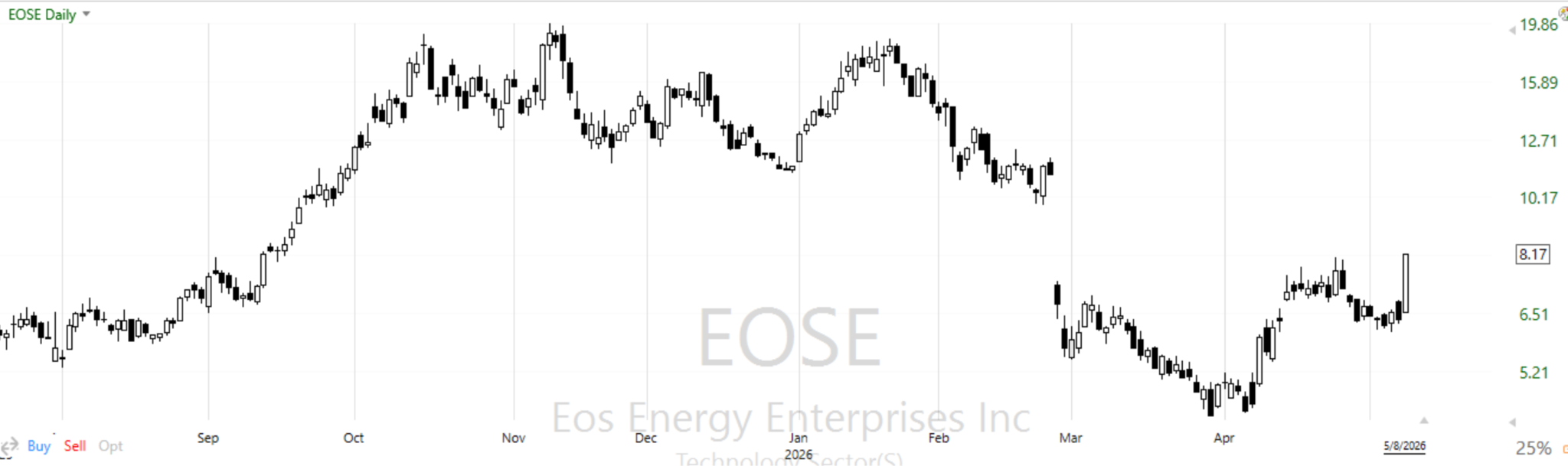

6/ Eos Energy Enterprises (EOSE)

EOSE uses a proprietary technology to develop zinc-bromine energy storage systems. They’re an alternative to lithium-ion batteries.

EOSE’s moat is being able to bypass the expensive clean rooms which are standard for lithium-ion production. It only needs 5 cheap and recyclable raw materials:

Zinc bromide

Graphite

Titanium

Plastic

Water

The materials are common, and EOSE sources them within a day-long drive from its Pennsylvania facility.

So the batteries are based on zinc bromide and water. This leads to three massive advantages given that EOSE’s clients are datacenters:

1/ They’re non-flammable and therefore safer.

2/ There’s no dendrite problem because the zinc platelets can dissolve back in the aqueous solution. The batteries are expected to operate for more than 20 years with minimal degradation.

3/ EOSE’s supply chain is domestic, which means it profits from tax incentives and is immune to tariffs.

This is all nice and clear but the stock still collapsed massively after the earnings report in February. It was a double miss on both revenue and earnings.

Then the stock continued falling and then abruptly reversed in March. Public filings show that two directors and CEO added 115,150 shares close to the bottom in March. The stock is recovering now.

The problem with EOSE was that they were losing money on every battery shipment.

In 2024, it cost them $6 for every $1 in revenue (gross margin -500%). By 2025, Line 1 of its facility in Pennsylvania scaled, and they reduced the costs to $2,20 for every $1.

It still wasn’t optimal but the trajectory was right.

In April, EOSE posted a preliminary report for Q1 2026 where further improvements are explained:

86% reduction in material travel distance

40% reduction in line length

22% jump in automation yields

This means EOSE will spend less to produce more. In addition, a second battery line (Line 2) passed its factory acceptance testing and should come online by the end of Q2 2026. This is important because EOSE could achieve a positive gross margin this year by scaling its production. A backlog of $701,5 million will help.

A recent development is EOSE’s partnership with TURBINE-X Energy that provides gas turbines. The goal is to help secure energy supply to new datacenters within months, not years before they’re connected to the electric grid.

This could be done by TURBINE-X Energy alone. However, even if a site has a stable energy supply, EOSE involvement is essential.

Gas turbines operate best at a steady output while EOSE batteries absorb excess power when datacenter demand is low and discharge it during peak hours.

This is especially important for AI inference because it creates energy spikes. EOSE batteries can respond within 3-5 milliseconds which is faster than typical industrial storage systems.

EOSE reports on May 13. It’s been brutal to hold this stock. We’ll soon find out if it’s been worth it.

7/ Uber (UBER)

UBER is a global technology platform and transportation company involved in ride hailing, food delivery, and freight transport.

The company’s latest earnings report makes it clear it remains committed to its AV strategy:

Revenue up 10% YoY (on a constant currency basis)

Gross bookings up 21% YoY

Monthly active users up 17% YoY

Adjusted EBITDA up 33% YoY

Free cash flow $2,3 billion

Cash balance $6,1 billion

Operating income up 57% YoY

GAAP net income $263 million

The net income was affected by a reevaluation of UBER’s pre-tax equity investments which resulted in a $1,5 billion reduction. This is just a nice way to say UBER’s investments in similar businesses suck. The reduction doesn’t come from UBER’s operations.

These are the highlights from the latest quarter:

1/ 50 million Uber One users

2/ The Delivery segment grew the most, by 23% YoY, Mobility grew by 20%, and Freight by 6% YoY.

3/ Outlook for Q2 2026:

Gross bookings $56,25 billion to $57,75 billion (up 18% to 22% YoY).

Non-GAAP EPS $0,78 to $0,82 (31% to 38% YoY).

Adjusted EBITDA $2.70 billion to $2.80 billion.

CFO Balaji Krishnamurthy noted that UBER is

“... taking a capital-efficient approach to AVs and embracing AI to drive growth and productivity.”

We can infer two points from here: UBER remains an asset-light platform and it has enough cash to invest in the platform. In other words, UBER stays committed to its original plan: It doesn’t want to own the AVs, it only wants to manage them.

There’s a caveat, though. UBER must’ve realized if it doesn’t help car manufacturing companies with AVs, it’ll miss the train.

This is the reason it’s using its massive cash balance to secure a supply of AVs without purchasing the AVs. This is mostly clearly seen in its partnership with Lucid as of Q1 2026:

1/ It expanded from 20,000 to 35,000 vehicles

2/ UBER is allocating $500 million instead of the $300 million planned initially

3/ UBER Chief Product Officer Sachin Kansal was nominated to Lucid’s Board of Directors

In other words, UBER is no longer just a partner but also an architect of Lucid AVs.

Uber has a number of other partnerships with companies developing AV technology (Zoox, Rivian, WeRide, Pony.ai, Waymo, and Hertz).

I’ve been long UBER since 2021.

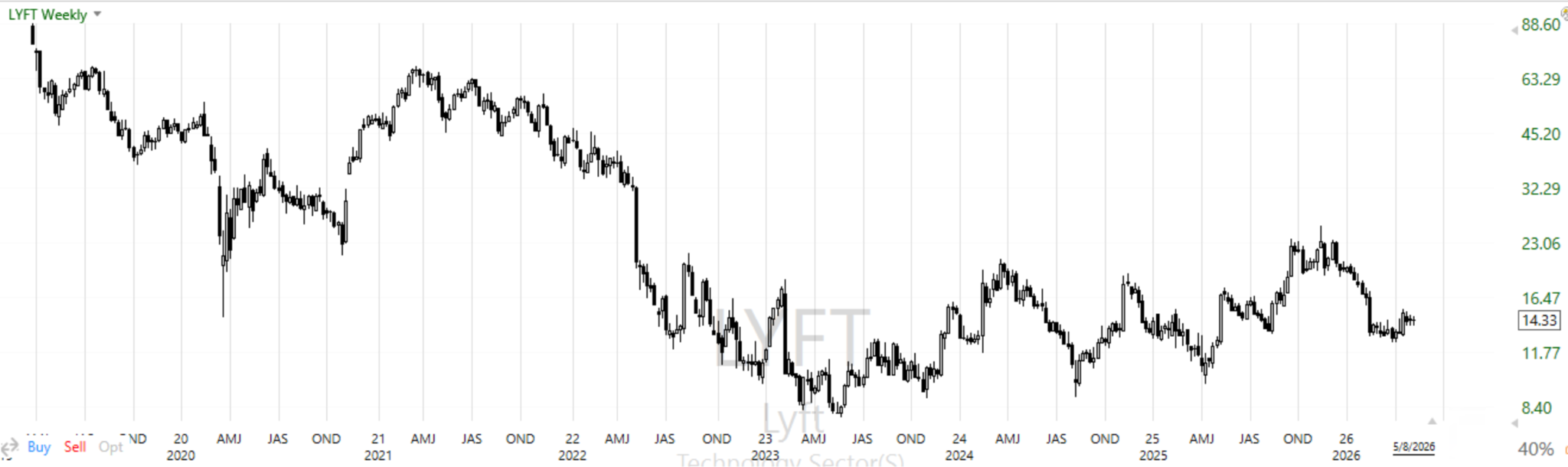

8/ Lyft (LYFT)

I bought LYFT at the same time as UBER in 2021. And well, the market proved me wrong a few months later.

I should’ve sold the stock and moved on but I decided to wait. When LYFT finally turned profitable in Q4 2024, I thought the stock would soar. It hasn’t happened yet, probably because the net income hasn’t been high enough (it’s fluctuating between $2 million and $60 million per quarter).

Financials from the earnings report on May 7:

Revenue up 14% YoY

Gross bookings up 19% YoY

Active riders up 17% YoY

Adjusted EBITDA up 25% YoY

Free cash flow $287 million

Cash balance $1 billion

GAAP net income $14,2 million

The growth metrics (in %) are comparable with UBER’s but LYFT stock just won’t grow.

Lesson from here: Don’t invest in young IPOs unless they’re already profitable. They IPO for a reason (to raise capital). It’s about survival. So the stock isn’t worth your money.

9/ New position: IonQ (IONQ)

IONQ develops and manufactures quantum computers based on trapped ions.

This technology is somewhat easier to implement as the computers operate at room temperature. In contrast, the quantum computers based on superconductors (like those developed by D-Wave Quantum, Google, and IBM) require extreme cooling close to absolute zero or minus 273 degrees Celsius.

The heart of IONQ’s machines is the quantum chip. It has about 100 electrodes that create electromagnetic fields and above which ytterbium or barium ions are suspended in a vacuum.

The ions themselves need to be cooled down to a temperature close to minus 273 degrees Celsius but this can be done using lasers that shine onto the ions. The rest of the setup is at room temperature.

You manipulate the states of those ions to solve computational problems.

However, the advantage of operating at room temperature comes at a cost.

Superconducting qubits operate in nanoseconds while IONQ’s gates operate in microseconds. When IONQ begins to operate millions of qubits, its computers could become relatively slow compared to superconducting quantum computers.

This doesn’t mean one or the other type of quantum computers will be useless, it just means they’re better suited for solving specific problems. IONQ already has customers like AstraZeneca and financial services companies.

I need to say that no company in the quantum computing space has a generally useful quantum computer yet. Everyone is doing R&D.

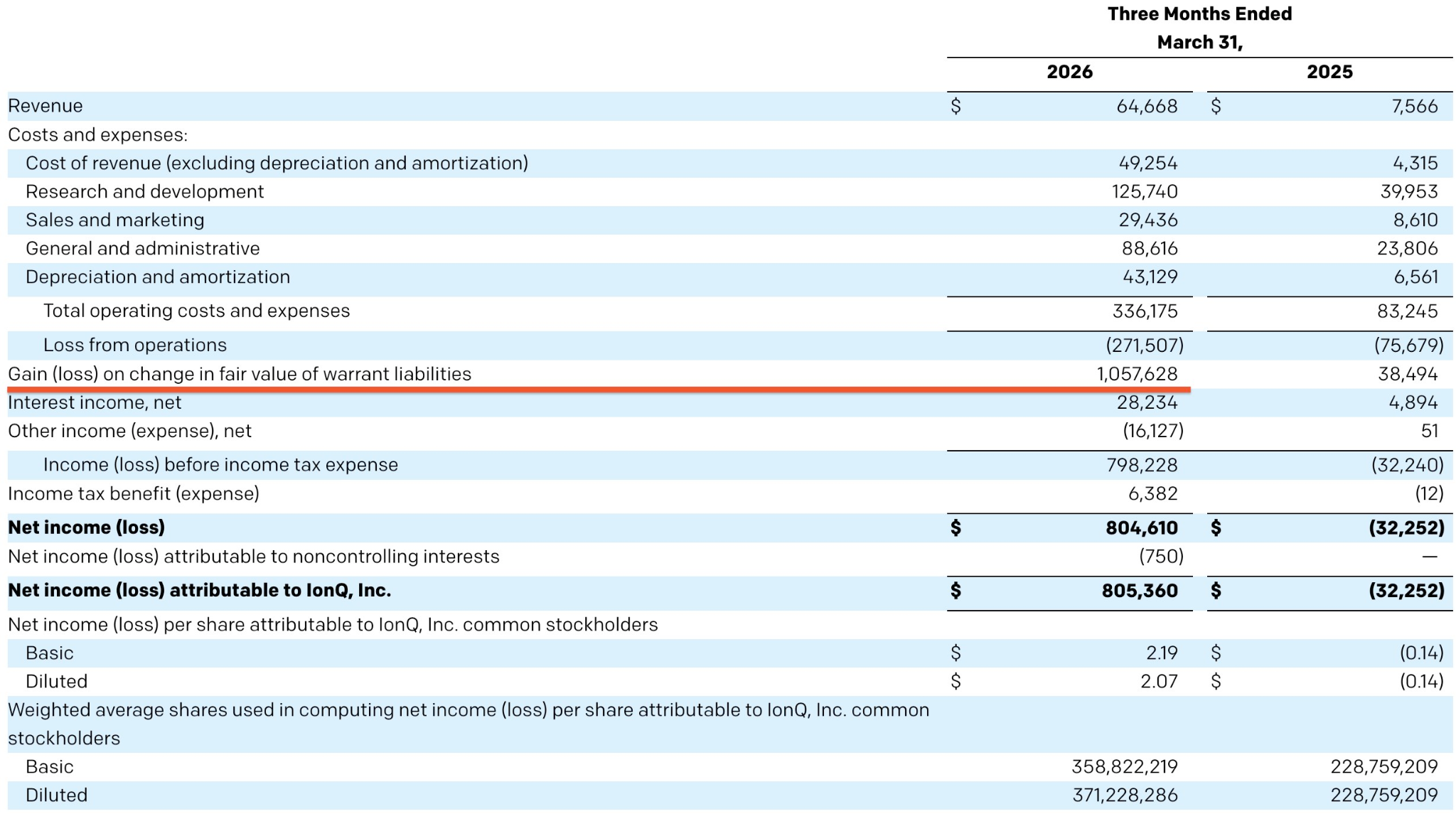

IONQ is slowly moving from R&D to enterprise. Recent financials show this:

Revenue up 755% YoY

Backlog $470 million (up $554% YoY)

Cash balance $3,1 billion

The revenue growth is great but we’re comparing relatively low figures: $7,5 million in Q1 2025 vs $64,7 million in Q1 2026.

I’m more impressed by the remaining performance obligations (backlog). The result is IONQ raised revenue guidance to $270 million for 2026 (up 107% YoY).

One interesting detail from the latest earnings report is IONQ booked a massive GAAP net income ($805,4 million). But the company is not operationally profitable yet.

The figure comes in large part from warrant liabilities worth $1,057 million. This is a non-cash gain (it doesn’t come from operations).

Like for SOUN, those warrants are rights for investors to buy stock at a certain price. That’s typically a lower price than the market price. The warrants are a liability.

Because IONQ was correcting most of Q1 2026, the value of this debt went down, and it appears that IONQ made more money than it really did.

Look at adjusted EBITDA loss ($96,8 million) to see the full story. That’s the figure that comes from operations.

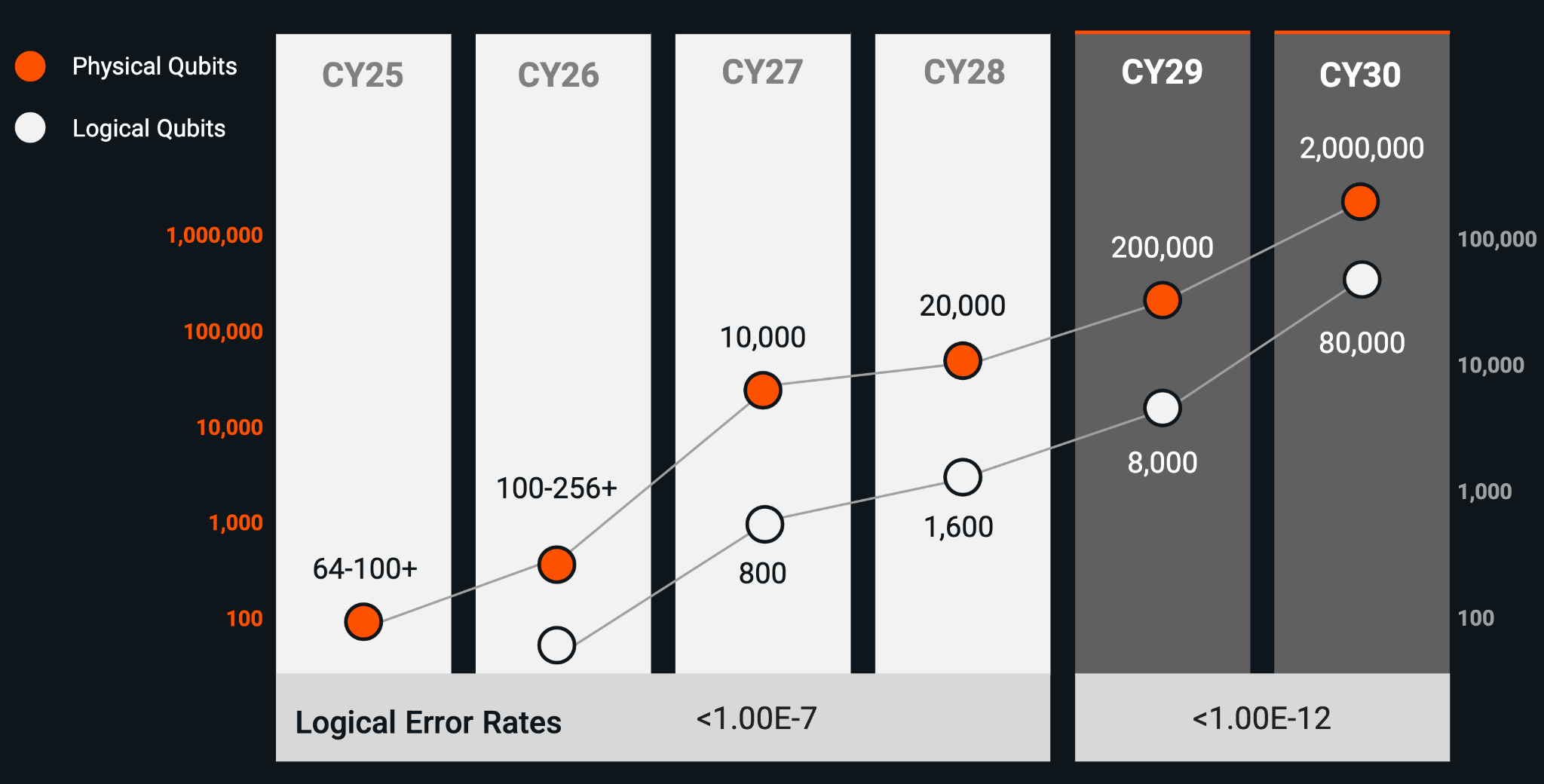

I’m bullish on IONQ but there’s one thing I’m missing in its reports and news releases: Logical qubits.

The qubits are ytterbium or barium ions. Adding more ions to the system is easy but entangling them (=making them sense each other) is not.

Ideally, every single qubit should be a logical qubit but that’s impossible. Qubits are fragile and can be perturbed by temperature instabilities, electromagnetic field instabilities, and vibrations. This leads to errors.

This makes their manufacturers introduce error correction algorithms. The algorithms involve data from more than one qubit. As a result, we distinguish between physical and logical qubits.

IONQ says it needs about 16 physical qubits per one logical qubit whereas superconducting computers would need about 1,000 physical qubits per one logical qubit. The reason is IONQ’s high two-gate fidelity (accuracy) of 99,99%. It’s like the error is there but you need to put in less time to correct it.

Here’s the problem: IONQ hasn’t demonstrated logical qubits yet. I admit it’s a hard thing to do. However, the company is already selling access to quantum computers through the cloud (AWS, Azure, Google) and standalone systems.

IONQ must demonstrate logical qubits. Its roadmap shows that IONQ expects 800 logical qubits in 2027. There’s no definite figure for 2026, however, IONQ promises to demonstrate a system which comprises 256 physical qubits.

In Q1 2026, IONQ sold the first 256 qubit system to the University of Cambridge. I assume the people in Cambridge know what they’re buying. In this press release, IONQ said it’d demonstrate the 256 qubit system in 2026. I’m interested in seeing this demonstration.

All this makes me cautiously optimistic on IONQ. I opened a small position this week.

The boring (and largest) part of my portfolio

I love following stocks but the foundation of my portfolio is 5 dividend ETFs and Bitcoin.

The ETFs are these:

1/ Invesco EURO STOXX High Dividend Low Volatility UCITS ETF Dist

2/ iShares STOXX Global Select Dividend 100 UCITS ETF (DE)

3/ Vanguard FTSE All-World High Div Yield UCITS USD

4/ VanEck Morningstar Developed Markets Dividend Leaders UCITS ETF

5/ SPDR S&P Global Dividend Aristocrats UCITS ETF

I add to them once a month. They were rising substantially until March and then stabilized.

I also have Bitcoin which I stopped adding to in October 2025. The latest Bitcoin winter is over. We’re at the beginning of the next Bitcoin bull market.

My current portfolio distribution:

Dividend ETFs: 48%

Individual stocks: 13%

Bitcoin: 39%

This was the state on March 1, 2026 from this post:

Dividend ETFs: 55%

Individual stocks: 11%

Bitcoin: 34%

Final words

The recent market volatility has made me question my investment theses a few times. But I see no reason to trim or sell my positions.

The Saaspocalypse is a popular topic these days. SaaS companies are growing their revenues and earnings while the market remains skeptical because “AI will kill them.”

Energy stocks have experienced wild swings as even a minor operational inefficiency can cause them to lose 40% a day.

I remind myself that volatility is not a bug, it’s a feature. If I want to make money in the stock market, I should be OK with the market challenging me.

After a while you begin to take volatility for granted. That’s how you sit out occasional corrections and stay invested long-term.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.

P.S. I’m always on the lookout for public companies with growth potential. If my stock picks resonated with you, hit Subscribe. I’ll keep you updated and give you new investment opportunities.

"Thesis hasn't changed" is the most expensive sentence in a portfolio review. Sometimes it's true. Sometimes it's the thing you say to avoid the work of actually re-running the thesis against the new numbers. The check isn't whether you'd buy more — it's whether you'd open the position today knowing what you know now.