3 Little-Known Stocks That Trillion-Dollar Investors Are Snagging

Time to look for bargains with them

Don’t reinvent the wheel if you want to get wealthy. Just do what the wealthy do.

People follow this advice in real life but forget it in capital markets. If you want to make money from investing, follow the most dominant market participant group - institutional investors.

BlackRock alone has $11,6 trillion in assets under management. It’s the wealth of the American middle class.

These kinds of companies don’t speculate or make emotional financial decisions. They know which stocks are undervalued, and their analysis goes way beyond P/E ratios.

Here are three stocks under accumulation by institutional investors.

1. This healthtech got punished for low guidance

Doximity ($DOCS) is the LinkedIn for medical professionals. It’s changing the future of telemedicine.

The platform has all you need as a doctor. You can upload your CV, training, certifications, and research. The app learns what you do and shows you ads and medical research relevant to your field.

Plus you can streamline your work by using the platform to stay in touch with your patients and colleagues. You can

Sign documents electronically

Contact a colleague to get a second opinion

Conduct patient visits via audio and video calls

Doximity makes money from subscriptions, advertising, job postings, and video calls through the platform. All are recurring revenue sources.

The financials of this profitable company are solid:

Revenue up 20% YoY

No long-term debt

Free cash flow $267 million, up 50% YoY

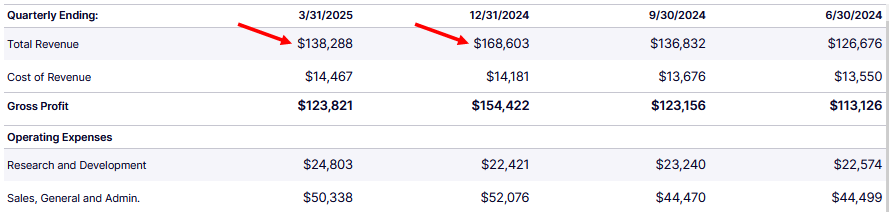

It could seem like there is an issue with the revenues lately.

The spiking revenue from the previous quarter is due to seasonal patterns.

The platform’s enterprise clients (hospitals and pharma) commit their annual budgets at the end of the year. Doximity also manages to sell additional workflow tools and expand marketing campaigns for its clients.

Both factors boosted the revenue at the end of 2024.

January-March are usually lighter quarters for Doximity. But the company is on a growth trajectory as the number of doctors registered on the platform (580k in Q4 2024 vs 620k in Q4 2025) shows. The total number of medical professionals using Doximity is almost two million.

I talked about Doximity in December 2024. The stock soared due to the good earnings report in February, then tanked in May.

How bad was the earnings report in May? The only negative I see is the “low” guidance (revenue growth 9% YoY).

Is the 10% drop on the day of the report justified? No, and the long white candlestick reflects the mistake of the traders who sold the stock off.

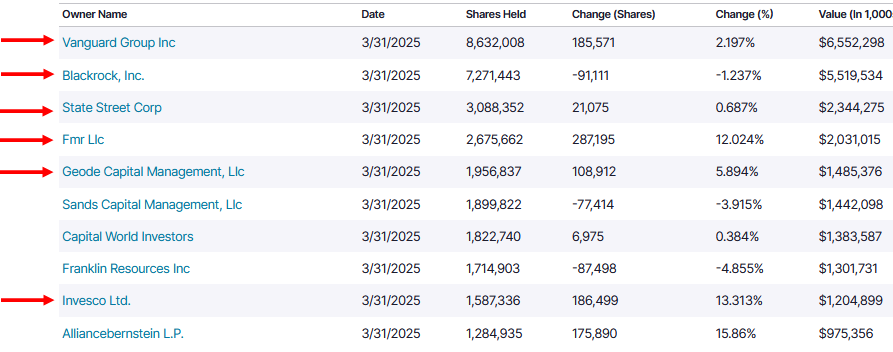

The long candle comes from institutional investors who supported the stock when the market panicked. $DOCS stock is coming back.

Institutional investors were buying $DOCS stock at higher prices before March 31, 2025.

No surprises here.

The number of Doximity’s users is on the rise, its revenues are growing, it has expansion opportunities in markets beyond the US, and it uses AI to optimize workflow, marketing, and compliance features.

Doximity stock is undervalued.

2. Here’s who helps keep you safe

The Aerospace & Defense industry is profiting from the increased spending on defense and public safety under the new US administration.

Axon Enterprise ($AXON) is a public safety technology company. Its initial brand was Taser, a non-lethal weapon for subduing suspects.

Now Axon’s business model is diversified. It provides

A records operating system

Real-time AI transcription tools

Body-worn and in-car cameras

Virtual reality training for the police force

Secure storage, access, and sharing of video footage

Drones and automated license plate readers for aerial and field intelligence

I’ll dare say the demand for Axon’s products and services is permanent whichever country you live in.

Axon’s customers are law enforcement agencies, corrections, the military, and private security customers in the US and beyond. No single customer exceeds 10% of Axon’s revenue.

The company is riding a $129 billion total addressable market in US law enforcement where its penetration is a mere 15%. And 2024 was a third consecutive year of 30%+ annual revenue growth.

Axon’s financials from last year:

Revenue up 33% YoY

Long-term debt $1,7 billion

Free cash flow $250 million YoY (estimate)

Axon focuses on software and domestic production. It’ll be minimally affected by the tariffs if this issue arises again.

The stock is already pricey. Yet the largest asset management companies keep buying it.

Axon keeps bringing new products to the market. Here’s what it announced in the latest earnings report:

Axon vehicle intelligence introduced new cameras for automated license plate reading, live streaming, and vehicle recognition.

Axon Assistant is a voice-activated AI solution that helps officers retrieve information without diverting their focus from the scene. The solution also supports over 50 languages. It is embedded in a body camera.

Axon Fuses is a real-time crime center platform that uses AI to give law enforcement a unified view of incidents and respond more effectively.

More growth is ahead.

Speculation is obvious recently in the stock chart. If I wanted to buy $AXON stock, I’d wait for it to calm down, perhaps retrace a bit, and move sideways for a few weeks.

It’s a good idea for Axon to split the stock so more investors can buy it. Stock splits tend to be preceded by price run-ups.

Axon was added to the Nasdaq index in December 2024 along with Palantir.

3. You don’t see what happens behind the scenes when you eat out

Restaurants are complex businesses. Just think of payments, payroll, takeout, insurance, accounting, recruiting, inventory, websites, marketing…

The company called Toast ($TOST) offers a vertically integrated platform for restaurant operations. Toast doesn’t rely heavily on third parties but designs and sells its own hardware, software, and payment processing system.

As of June 2025, Toast serves 140k restaurants from quick service to fine dining establishments. Its platform has tools for ordering, delivery management, payroll, marketing, and customer engagement.

Toast uses AI to help restaurants boost sales. The AI analyzes products, recommends order upgrades to customers, and improves efficiency.

The platform’s adoption is reflected in Toast’s financials:

Revenue up 27% YoY

No long-term debt

Free cash flow $69 million in Q1 2025

The company has three revenue streams:

Subscription to its software (recurring)

Payment processing fees as restaurants use Toast’s proprietary payment network

Hardware sales terminals and kitchen display systems. It’s the smallest revenue source but it’s crucial for onboarding new clients into Toast’s ecosystem

Most institutions were buying Toast stock last quarter. That’s a vote of confidence.

Toast has growth potential. Last quarter it added 6k locations and signed agreements with Applebee’s and Topgolf to set up Toast’s technology in their locations.

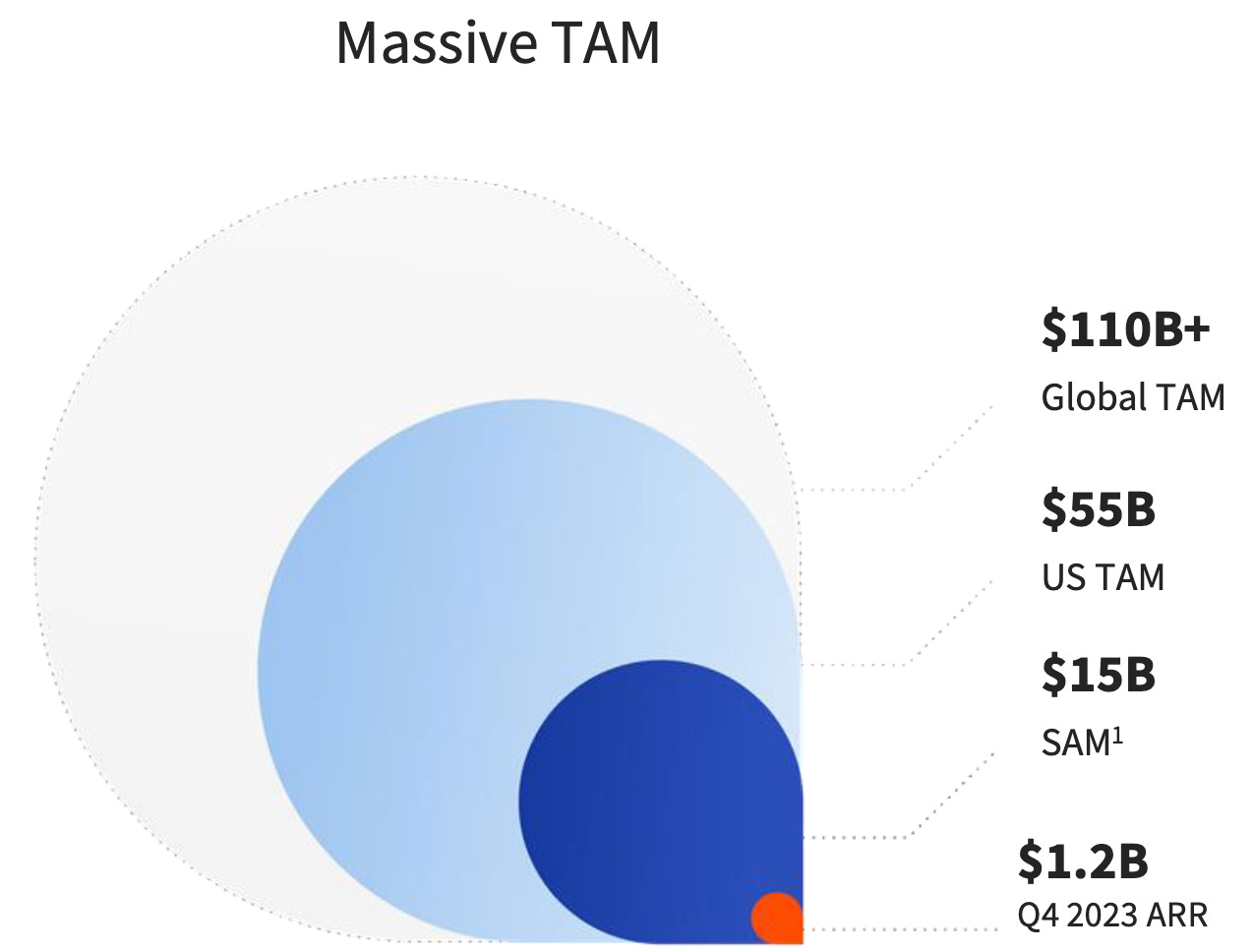

Here’s what Toast says about its total addressable market (TAM):

$TOST is a young public company. Its technical patterns are improving. The stock looks to complete the initial bottom at $65.

The improving stock chart reflects the company’s profitability over the past four quarters.

If you decide to buy $TOST stock, the best is to wait until the bottom has completed. But if your risk appetite is higher, you could enter sooner.

There could be price swings ahead but the rising revenues, profitability, and institutional interest will minimize them.

Final thoughts

There are always bargains in the stock market.

The obvious winners of the new tariff situation are service-oriented companies. Most of them develop software like Doximity and Toast.

Other businesses profit from increased spending on their niches like Axon.

If you want to find companies with growth potential, keep an eye on what institutional investors are buying. Their bargain hunting will show you what to invest in.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.

P. S. I send this newsletter twice a week. If you want to find more long-term investing opportunities backed by institutional money, hit the subscribe button.

You're an endless repository of knowledge on all things financial, Denis. Solid))